Double materiality is the latest buzzword in sustainability, referring to how the environment impacts a company and how the company’s activities affect the ecosystem in which it operates. Here, we break down this new perspective on issues that matter to stakeholders.

Businesses don’t operate in a vacuum. They are embedded within an environmental and social ecosystem that they both influence and are influenced by. In this reality, materiality is a key concept for understanding a company’s relationship with its surrounding environment. Ana Palao, Customer Experience Director at Sygris and a sustainability specialist, defines materiality as “the process of identifying and prioritising the sustainability issues with the greatest relevance and impact for both the company and its stakeholders.” In other words, it concerns which issues matter most to shareholders, employees, or social groups.

To the confusion (and even frustration) of many business leaders, the concept of materiality has expanded in recent years. What was once “materiality” on its own has now evolved into double and even triple materiality. But what does this new definition entail?

How does climate affect a company’s finances?

There have been several key milestones in the evolution of materiality. Until 2019, materiality was defined purely from a financial perspective. In June 2017, the G-20 Financial Stability Board published a set of recommendations on how financial institutions and companies should report their climate-related financial risks and opportunities.

Ana Palao, Customer Experience Director at Sygris: “Materiality is the process of identifying and prioritising the sustainability issues with the greatest relevance and impact for both the company and its stakeholders.”

The document, prepared by the Task Force on Climate-related Financial Disclosures (TCFD), focused on improving the disclosure of financial information related to global warming. “Financial markets need clear, comprehensive, high-quality information on the impacts of climate change. This includes the risks and opportunities presented by rising temperatures, climate-related policies, and emerging technologies in our changing world,” explains the TCFD on its website.

These recommendations have been widely accepted by many countries and companies as a global standard for reporting climate-related financial information. The TCFD’s perspective is from the outside in—focusing on how climate change might affect the value of companies.

Double Materiality

In 2019, the European Commission introduced the term “double materiality” in its Guidelines on reporting climate-related information, adding an inside-out perspective on how companies impact their surroundings. Thus, double materiality can be understood as:

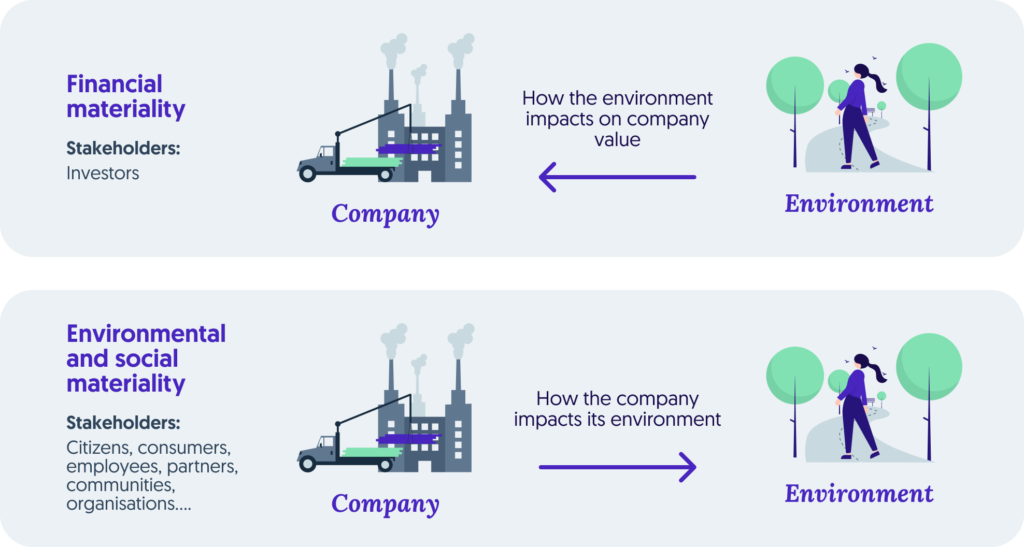

- Financial materiality: These are issues that affect the development, performance, and position of a company, relating to how external factors might impact its value. For example, how global warming or pollution might influence a company’s operations. The stakeholders most concerned with these issues are investors. This is the outside (environment) to inside (company) perspective.

- Environmental and social materiality: These are issues related to the company’s impact on its surroundings, particularly the environment and people. The stakeholders most interested in these matters include citizens, consumers, employees, business partners, local communities, and civil society organisations. However, investors are also increasingly concerned, as demonstrated by the growth of sustainable investment in recent years.

Nested and dynamic materiality

But materiality can become even more complex. At the end of 2020, the five leading sustainability standards organisations—Carbon Disclosure Project (CDP), Climate Disclosure Standards Board (CDSB), Global Reporting Initiative (GRI), Integrated Reporting Framework (IIRC), and Sustainability Accounting Standards Board (SASB)—took the concept further by publishing a triple materiality perspective in their report Statement of Intent to Work Together Towards Comprehensive Corporate Reporting. They divided material issues into three groups:

- Issues that reflect significant impacts of the organisation on the economy, environment, and people. These are of interest to users with diverse goals who want to understand the company’s positive and negative contributions to sustainable development.

- Sustainability issues that are material for the company’s value creation. These are relevant to users whose main objective is to enhance the company’s economic decisions. This group is a subset of the first group.

- Issues already reflected in the organisation’s financial statements, including cash flow projections and assumptions. This is a subset of the second group.

From this perspective, materiality is “nested” because each subgroup is contained within the one before it, with all falling within the first group that addresses impacts on the economy, environment, and people. Additionally, it is “dynamic” because issues can move from one group to another and eventually become financial in nature.

CSRD and Double Materiality

Since 2021, the importance of double materiality has grown, especially with the implementation of the Corporate Sustainability Reporting Directive (CSRD) by the European Union in 2024. This regulation requires more companies to disclose detailed sustainability information, considering both financial and non-financial impacts.

In the context of decarbonisation, if GHG emissions are a material issue for a company, it is essential to develop an emissions management strategy and decarbonisation plans. The EU, through the European Green Deal and the Fit for 55 package, has set targets to reduce GHG emissions by 55% by 2030 and achieve climate neutrality by 2050, making emissions management strategies crucial.

Moreover, there has been an evolution towards “triple materiality” integrating economic, social, and environmental impacts into a more holistic and interconnected view. This shift reflects a global trend towards transparency and responsibility in sustainable business management.

Introduction of Omnibus Project

The recent introduction of the Omnibus Law by the European Commission aims to simplify and reduce the administrative burden associated with ESG regulations. Among the proposed measures, the revision of the Corporate Sustainability Reporting Directive (CSRD), the EU Taxonomy, and the Corporate Sustainability Due Diligence Directive (CS3D) stands out. This includes reducing the number of companies required to comply with these sustainability requirements, exempting those with annual revenues below €450 million. At first glance, this may seem to impact preliminary consultancy exercises. However, nothing could be further from the truth.

Although the Omnibus project might initially appear to significantly limit the scope of ESG reporting requirements for certain companies, it should not be interpreted as an opportunity to abandon or relax the rigour of double materiality analysis. On the contrary, this methodology remains crucial, not only from a regulatory compliance perspective but also strategically and competitively.

Double materiality allows for a comprehensive analysis of how a company both impacts and is impacted by environmental, social, and governance issues. Although the Omnibus project might initially exempt certain companies from reporting impacts according to some of the stricter ESG criteria, abandoning this practice would mean losing a key tool for anticipating future regulatory changes and maintaining competitive advantage in a market where consumers and investors increasingly value transparency and sustainability commitments.

Furthermore, employing internationally recognised methodologies, such as the Value SME (VSME) methodology, lends rigour and credibility to the analysis. This approach not only facilitates potential compliance with future regulations that may naturally evolve from Omnibus but also enhances the company’s positioning and public perception. Companies proactively committed to ESG transparency and responsibility tend to be better prepared to manage emerging risks and seize sustainability-related opportunities.

From a strategic viewpoint, continuing to apply double materiality analysis helps clearly identify aspects that could represent material risks or significant opportunities for the business in the medium and long term. Regardless of immediate exemptions that Omnibus might provide, companies that adopt these reporting practices early will be better positioned to swiftly adapt to future regulatory changes and capitalise on opportunities emerging from new sustainable markets, improved relationships with conscientious investors, and committed customers.