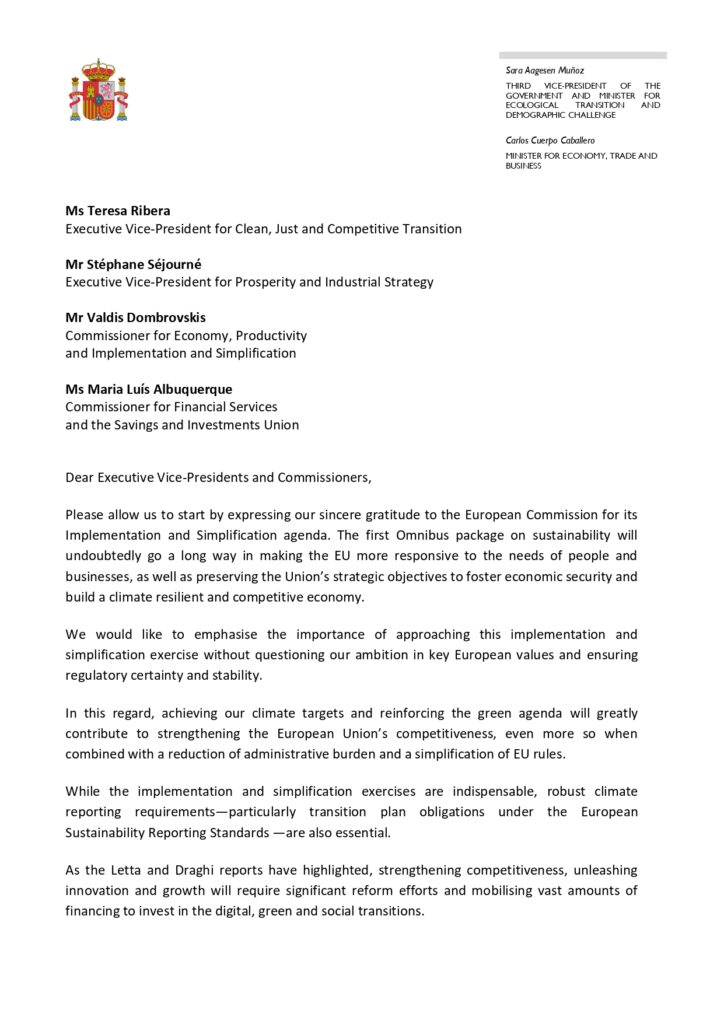

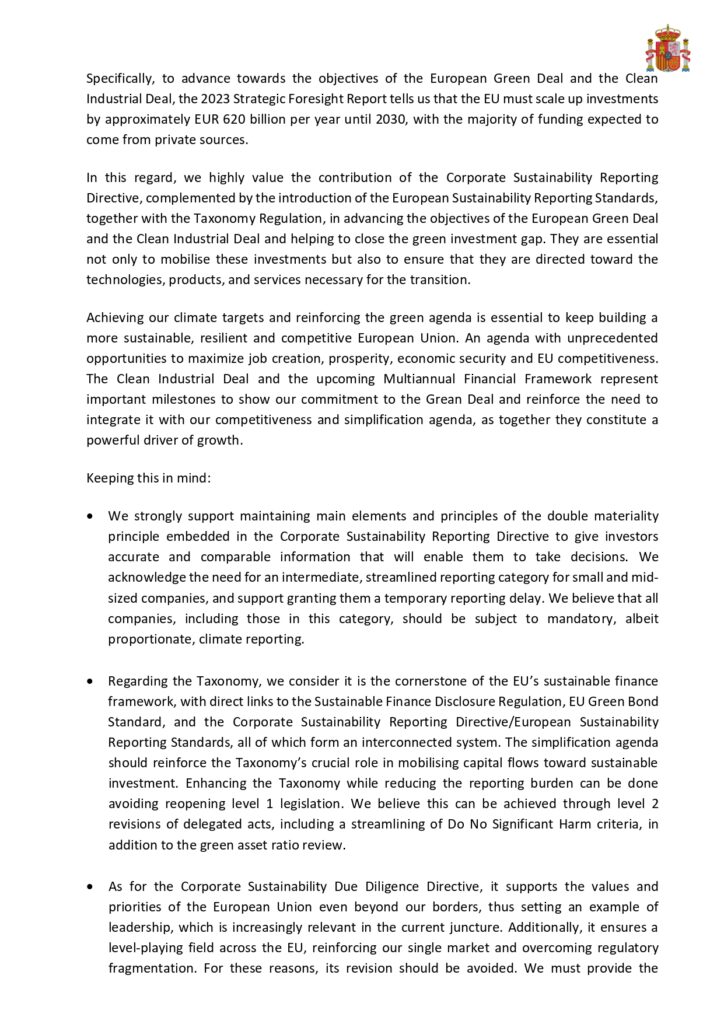

The Spanish government has taken a firm stance against any attempt to roll back the implementation of the Corporate Sustainability Reporting Directive (CSRD). In response to recent discussions regarding a possible relaxation of reporting requirements within the EU, Spain has sent a letter to the European Commission urging it to uphold the commitments made on sustainability and corporate transparency.

What is happening with the CSRD?

The CSRD is a key pillar of the European Union’s sustainability agenda. Its objective is to ensure that companies provide detailed and verifiable information about their environmental, social, and governance (ESG) impact. Through this directive, the EU aims to foster a more transparent economy, aligned with the principles of the European Green Deal and the bloc’s climate commitments.

However, in recent months, voices within the European Union have called for a relaxation or reduction of the CSRD’s requirements, arguing that the administrative burden on businesses is excessive and could harm their competitiveness. In response to this possibility, Spain has reacted swiftly, making it clear that it will not support any weakening of the directive’s implementation.

Key points of the letter

In its letter to the European Commission, the Spanish government highlights the following key points:

Commitment to Sustainability: Spain considers the CSRD to be a fundamental tool for driving the transition towards a more sustainable and competitive economy. The government emphasises that corporate transparency in ESG matters is crucial for attracting investment and strengthening the resilience of the European market.

- Impact on the EU’s competitiveness: Contrary to arguments suggesting that the directive could undermine business competitiveness, Spain maintains that sustainability is a driver of growth and global leadership. Weakening the CSRD’s requirements would send contradictory signals to markets and investors, undermining the EU’s position relative to other economies advancing similar regulations.

- Investor confidence and access to finance: The letter highlights that transparency in sustainability is a key element in maintaining investor confidence. Clear and standardised ESG reporting enables businesses to access sustainable finance, such as green bonds and loans linked to sustainability criteria.

- No to legal uncertainty: Any regulatory change at this stage of the process would create uncertainty and confusion for both businesses and regulators. Spain insists that modifying the CSRD’s requirements now would jeopardise the coherence and effectiveness of the European regulatory framework.

- Alignment with the EU’s climate strategy: Loosening the CSRD’s requirements would contradict the objectives of the European Green Deal and the EU’s sustainable finance agenda. Spain argues that the green transition requires clear and comparable information, and that the current regulatory framework is the right mechanism to ensure this.

What could happen next?

Spain’s firm position increases pressure on the European Commission in this debate. However, it is still too early to determine how the situation will evolve. Some possible scenarios that could unfold in the coming months include:

- Review of the administrative burden: The European Commission could propose specific adjustments to simplify CSRD compliance, particularly for SMEs, without compromising the directive’s core principles.

- Maintaining the current regulatory framework: If support for the CSRD from Spain and other countries is strong enough, the Commission may decide to keep the directive unchanged, reinforcing its commitment to transparency and sustainability.

- Partial flexibility or staggered implementation: It is possible that the Commission could propose a more gradual implementation or sector-specific flexibilities to address concerns over the administrative burden.

- Greater dialogue with the private sector: In response to pressure from some businesses and industry associations, the EU may open new working groups to assess the real impact of the CSRD and explore alternatives to facilitate its implementation without undermining its objectives.

Spain has made it clear that it will not allow a regression in the EU’s commitments to sustainability and transparency. The CSRD is a key step in transforming Europe’s corporate landscape, and weakening it would pose a risk to the EU’s credibility and leadership in ESG matters.

The debate in Brussels remains open, but with several EU countries taking a firm stance, there is a strong likelihood that the directive will retain its core essence and continue to be a cornerstone of Europe’s sustainable transition.